The Business Owner's Year-End Tax Planning Checklist: 10 Moves to Make Before December 31

For business owners, the fourth quarter is the most critical time of year for tax planning. Once December 31 passes, most of your options disappear. The moves you make — or don't make — in the final weeks of the year can mean the difference of tens of thousands of dollars on your tax return.

At Big Life Financial, we help business owners implement year-round tax strategy. Here are the 10 most impactful moves to make before the calendar turns.

1. Maximize Retirement Plan Contributions

Maximize your solo 401(k), SEP IRA, or defined benefit plan contributions before year-end. For defined benefit plans, key actuarial elections must often be made by December 31. See IRS retirement plan deadlines for current limits and rules.

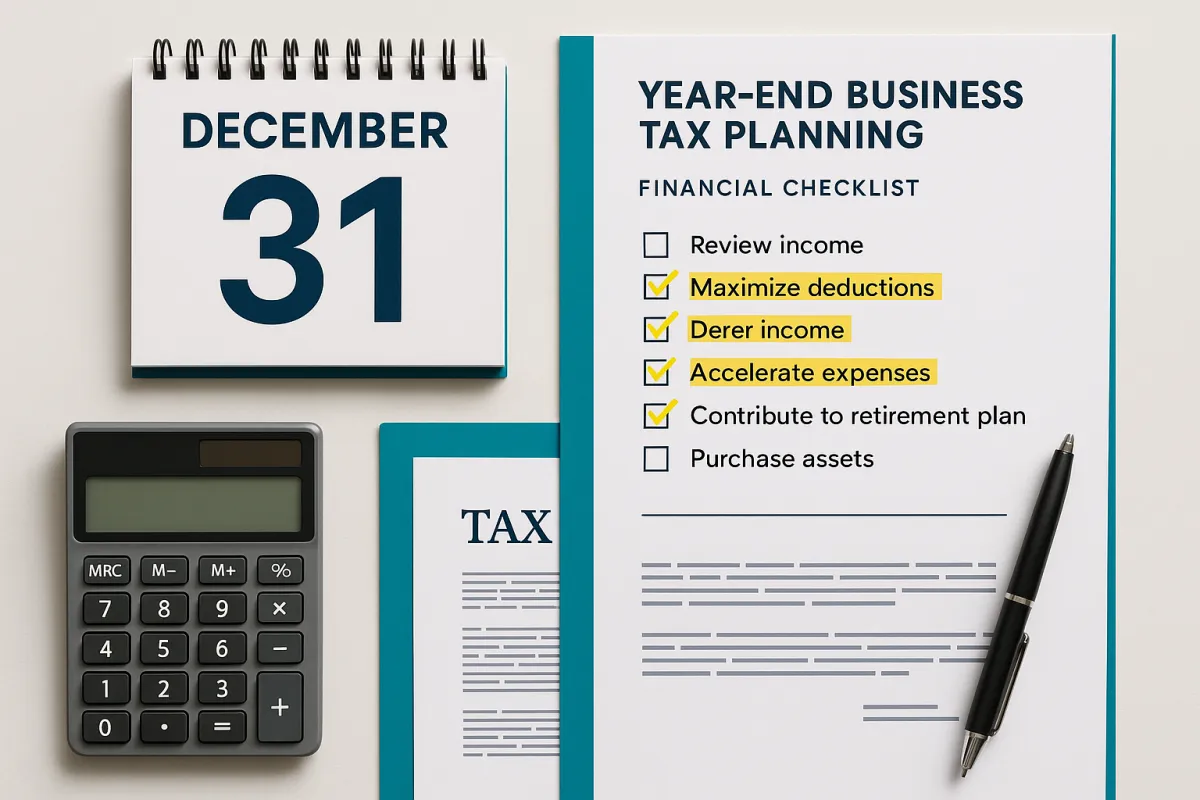

2. Accelerate Deductible Business Expenses

Need new equipment, software, or office upgrades? Purchasing and placing them in service before December 31 allows a current-year deduction. Under Section 179, businesses can immediately deduct the full cost of qualifying equipment up to $1.16 million in a single year.

3. Defer Revenue Where Possible

Cash-basis business owners can delay invoicing certain clients until January, pushing that income into the following tax year and providing valuable flexibility with your current-year liability.

4. Review Your Business Entity Structure

Is your current entity still optimal? Moving to an S-Corp or restructuring existing entities can create significant tax savings — but these decisions often need to be implemented before year-end to take effect for the current tax year.

5. Make Strategic Charitable Contributions

Donor-advised funds (DAFs) allow you to make a large, fully deductible contribution this year and direct grants to chosen charities over time — maximizing your tax deduction while maintaining complete flexibility in your giving.

6. Tax-Loss Harvesting in Investment Accounts

Review your portfolio for unrealized losses. Selling these positions to offset gains elsewhere in your portfolio reduces capital gains tax liability, while careful rebalancing preserves your overall investment strategy.

7. Fully Fund Your Health Savings Account (HSA)

If you have a qualifying high-deductible health plan, fully fund your HSA before year-end. Contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses.

8. Consider a Strategic Roth Conversion

If your income is lower than usual this year, a partial Roth conversion can be a powerful move — paying taxes now at a lower rate to create a tax-free income stream in retirement.

9. Execute the Augusta Rule

Have you held any documented business meetings at your personal residence this year? Under IRS Section 280A, you can rent your home to your business for up to 14 days annually tax-free. There may still be time to schedule and properly document qualifying meetings this year.

10. Schedule Your Year-End Tax Strategy Review

A focused review with a tax strategist who understands your business can identify opportunities worth thousands of dollars — opportunities that permanently disappear after December 31. Contact Big Life Financial now to schedule your year-end tax strategy session before time runs out.